Competition in banking – how big a problem is it?

Competition in banking – how big a problem is it?

Our measures of competition paint an ambiguous picture

Remember the joke that Canada is a stack of oligopolies in a trench coat, one of them being Canada’s so-called banking oligopoly? It’s more than a joke. It’s a conviction behind political promises. During the recent election, the Conservatives promised to increase competition in banking. The Liberals did the same and then some. They also proposed a bank tax, as if to say the banks’ profits are excessive, which would imply a competition problem because excessive profits are the fruits of excessive market power.

The idea that there’s a competition problem in Canadian banking is intuitively appealing, but the truth isn’t so straightforward. Though Canada’s big five banks control 85 percent of the country’s banking assets, market concentration isn’t necessarily evidence of a competition problem. In small markets where there are increasing returns to scale, uniformly distributing market share across hundreds of firms would be oppressively inefficient. Goods and services would be prohibitively expensive. Markets would shrink. Sometimes a few firms is all a market needs to work its competitive magic.

To get to the bottom of whether there is a competition problem in Canadian banking, we need better measures of competition than concentration. Jean Tirole, a Nobel prize winning economist, wrote that policymakers ought to worry about market contestability instead of market concentration. Market contestability is the idea that incumbents, whether they’re big or small, are at a non-trivial risk of being displaced by their competitors. When there is no market contestability, complacency creeps in and the wheels of competition stop turning.

Available measures paint an ambiguous picture

Economists have a few ways of guessing how contestable markets are. There’s the H-statistic, the Lerner index, and the Boone indicator. Don’t be intimidated by the arcane names. All you need to know is that these measures rely on basic economic theory to work. They try to measure the extent to which firms have so much market power that they can influence economic outcomes, which is a telltale sign of a competition problem. None of the measures is perfect, but what is?

The H-statistic suggests Canada’s banking sector is more competitive than the United States’, the United Kingdom’s, and Australia’s. Developed by economists James Panzar and John Rosse in the 1980s, the H-statistic tells us how sensitive banks’ revenues are to changes in their input costs. According to economic theory, if banking is perfectly monopolistic, banks’ revenues will fall when banks’ costs rise. Alternatively, if banking is perfectly competitive, then banks’ revenues will rise with their costs.

When the H-statistic is less than zero, it’s supposed to mean banking is monopolistic. When the H-statistic is equal to one, it’s supposed to mean banking is competitive. In between zero and one means firms have a moderate degree of market power because their products are not identical yet are imperfectly substitutable for one another. Coca Cola isn’t exactly Pepsi, for example, but either should suffice in the absence of the other.

Though Canada’s H-statistic is close to one, the H-statistic is flawed. Since Panzar and Rosse developed their measure, some economists have found that it’s not a reliable indicator of how competitive a market is. The reasons may put you to sleep, and so I won’t elaborate on them here. The upshot, however, is that one shouldn’t rely on the H-statistic because of how ill-behaved a measure it is.

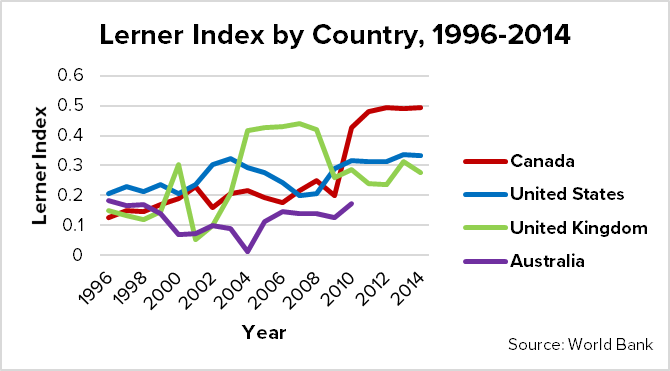

Here’s an example of the unreliability: if the H-statistic is relatively good news for Canadian banks, then the Lerner index is relatively bad news. The Lerner index is like a golf score: the lower, the better. According to the Lerner index, Canada’s banking sector is less competitive than the United States’, the United Kingdom’s, and Australia’s. The Lerner index says the opposite of what the H-statistic does, even though both are proxy measures of the same general thing.

Developed by economist Abba Lerner in the 1930s, the Lerner index measures the extent to which banks mark up their prices. The theory is that the more a firm can charge above its costs, the more market power that firm has. The higher you score on the Lerner index, the more market power you have.

The Lerner index, too, has its flaws. Economists have catalogued the reasons why a high score on the Lerner Index doesn’t necessarily equate to market power. For example, in markets with high fixed costs, a high score on the Lerner Index may just mean a firm is charging above its marginal cost to cover its fixed costs, not that it has so much market power that it can charge monopoly prices.

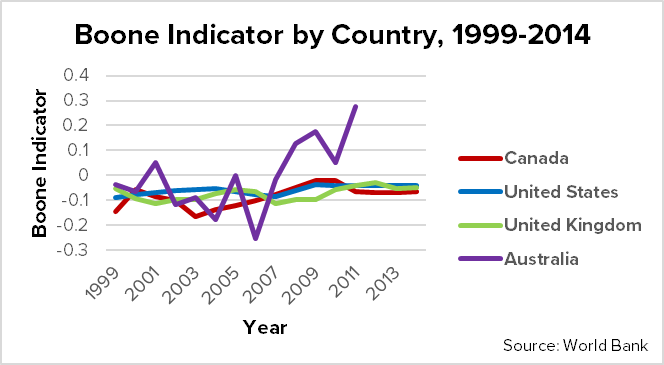

The Boone indicator is a newer measure of competition. Developed by Jan Boone in the late 2000s, the Boone indicator measures the sensitivity of banks’ profits to their marginal costs. The reason this matters is that more efficient firms should have lower marginal costs, and firms that are more efficient should earn higher profits. The more competitive a market is, the stronger the efficiency-profit relationship should be.

By this measure, Canada’s banking sector barely outperforms the others. The Boone indicator is also like a golf score: the lower, the better. When the Boone indicator is less than zero, it’s supposed to mean that high-efficiency firms are beating low-efficiency firms, which is what ought to happen in a competitive market. When it’s above zero, it’s supposed to mean that the market isn’t working as it ought to be.

Though Canada ranks ahead of its peers, Canada’s relative ranking isn’t exculpatory. Years ago, economist Michiel van Leuvensteijn tested the mettle of the Boone indicator. He checked whether it would reasonably measure the levels of competition in the United States’ sugar industry from 1890 to 1914, a span of time when the industry went from being dominated by a cartel to being trust-busted by regulators. During the most oligopolistic period, when the cartel almost had control of 100 percent of the market, the Boone indicator was at its highest: less than zero, like it is for Canada’s banks, but close to zero.

A problem well defined is a problem all but solved

You’ve heard the saying that it’s better to measure twice and cut once. Over the years, we’ve seen some research that tries to answer the question about competition in Canadian banking. But the research is either old or incomplete—or both. In Canada, I’m not sure we’ve adequately measured the extent of the problem even once.

More than a decade ago, Jason Allen and Walter Engert found that the Canadian market for banks was relatively competitive. But Allen and Engert’s paper relied on the flawed H-statistic to make the case. More recently, the Competition Bureau released a market study that identified regulatory barriers to fintech innovation in Canada’s financial sector, which make the market less contestable. But the mere identification of barriers to innovation tells us nothing about the magnitude of their effects. Moreover, the Competition Bureau’s study focused mostly on fintech innovation, illuminating little about whether the federal government’s approach to banking law and oversight makes things more or less competitive.

The truth is we don’t know the extent to which there is a competition problem in Canadian banking. The conviction with which people opine on the future of financial sector policy, let alone make actual policy, would be epistemically virtuous if it stood on the shoulders of evidence just as strong. So where is the evidence?

If you found this interesting, please like it, share it, or let our community of readers know what you think in the comments.