Field notes: January 2026

Switching banks, AI bubble, the U.S. politics of crypto, Tiff Macklem on non-bank financial institutions, and Mark Carney's speech

In the news

1. More Canadians switching banks…or are they?

Yes, with a footnote. About 24 percent of Canadians who switched financial services switched financial institutions as well last year. This is according to a survey by Environics Research. “In the 20 years we’ve been running this study, it’s the highest incidence ever of those switching a financial account,” said Heidi Wilson, vice president of financial services at Environics Research. The percentage of surveyed Canadians who switched institutions was 21 percent in 2023 and 2021, the two times survey was administered.

Over the past several years, Canada has seen an uptick in bank and non-bank competition, such as EQ Bank and Wealthsimple. Wealthsimple signed up 200,000 new customers last year after it officially launched its own suite of bank-like products, including a credit card. If the federal government’s budget-2025 proposals to increase financial-sector competition deliver as intended, then the competition is just going to get fiercer.

That said, it’s not actually clear how many Canadians are switching financial institutions.

On Environics Research’s landing page for the switching study, it says “nearly 6 million Canadians make the decision to switch one or more of their financial products,” as if the annual number hasn’t changed over the years.

Later on in the FAQ section, it says “1 in 4 Canadians switch financial products in a given year.”

Here’s what Hay International Research, the survey’s administrator before Environics Research took it over, says: “Year after year we find that about 1 in 5 Canadians switch one or more financial products over a 12 month period.”

Environics Research didn’t publish a report about the survey methodology or findings. All we know is about 45,000 people who sought out new financial services were surveyed. Questions remain about what the survey can really tell us about behaviour over time and how robust its findings even are.

2. Global economy is resilient, AI bubble may not be so bad

According to the IMF’s latest economic outlook, headwinds from destructive trade policies are meeting tailwinds from massive investments in AI. Fiscal and monetary policy are also helping. So is the private sector’s adaptability. At the first sign of geopolitical drama, companies were quick to reorganize supply chains and export to new markets. The net result seems to have been modestly positive: global economic growth is now expected to be 3.3 percent this year — revised upward from the estimate in 2025 — and 3.2 percent in 2027. That is, of course, if there isn’t a change in the winds.

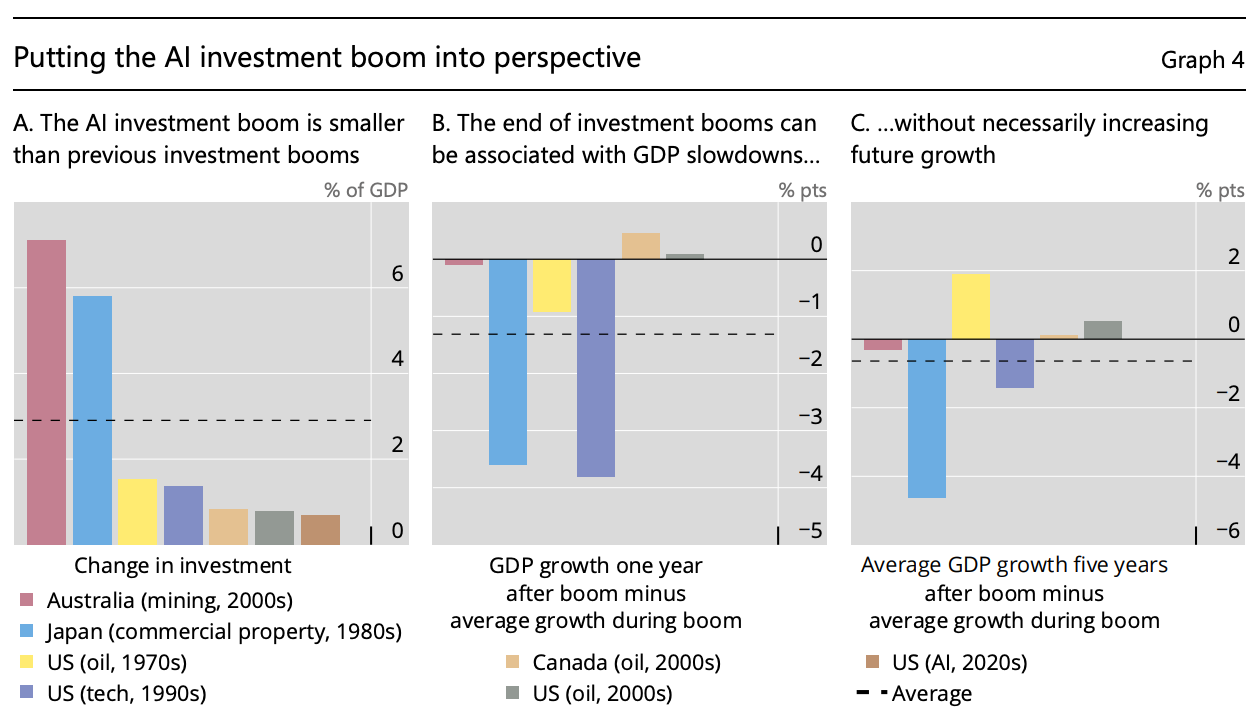

Still, even if the AI investment boom turns out to be a bubble, cautious optimism may be the most rational mood. According to one estimate, U.S. investment in data centres and chip production approached one percent of GDP in 2025. Wall Street may be bankrolling some of this investment with creative financing, obscuring the level of debt being incurred by big-tech borrowers, but the macroeconomic consequences of a bursting bubble may not be that big. Here’s how researchers from the Bank for International Settlements, the so-called bank of central banks, explained it:

The stakes aren’t high by historical standards. The level of investment in AI is “similar in size to the US shale boom of the mid-2010s,” wrote Aldasoro et al, “and half as large as the rise in IT investment during the dot-com boom of the 1990s.”

The level of AI-related debt isn’t comparatively alarming. While firms that are investing heavily in AI like Alphabet and Microsoft are relying on debt-financing to do it, they collectively carry less debt (relative to total assets) than other firms in the economy.

Risk is still being diversified. Private credit is a key source of financing for AI investments. More than 15 percent of funds were lending to AI firms in 2025, but the average share of lending allocated to AI firms was about 5 percent that same year.

That doesn’t mean an AI bubble bursting won’t hurt short-run growth. Quite the contrary, as Andrew Spence concluded one of his recent posts, “the economic undertow could be deep, long lasting and expensive to stabilize.” But as Alex Imas wrote, even if there is a bubble, the economic effects of AI may nonetheless be positive and exceed our expectations in the medium or long run. Not all bubbles are created equal.

We shouldn’t worry so much about bubbles bursting. Far more worrying is there not being any bubbles to burst. Because if bubbles are never bursting, then markets aren’t taking enough chances. And not taking chances is the surest way to the most enduring risk of all, which is death. More worrying for the global economy is the insidious effect of geopolitical chaos and institutional decay (and, as Dan Munro reminds us, incomplete assessments of costs and benefits).

3. The biggest risk to crypto industry is naive dogmatism

Speaking of institutional decay, Coinbase flexed its muscles in Washington, DC to pause a Senate committee vote on a bill that would comprehensively regulate digital assets, such as bitcoin. “After reviewing the Senate Banking draft text over the last 48hrs,” Brian Armstrong, CEO of Coinbase, posted on X, “Coinbase unfortunately can’t support the bill as written.”

Armstrong listed his grievances. He takes issue with the powers that would be given to the Securities Exchange Commission, which had been aggressively policing the industry in the Biden years. He doesn’t like the ban on yield-bearing stablecoins, a restriction supported by American banks. He appears to reject the idea that decentralized finance should be subject to current anti-money laundering and know-your-customer rules.

While lazy reporting made it seem like the crypto industry’s reaction to the bill was all the same, Coinbase may be more outlier than representative. For example, how would you read this post from Chris Dixon, managing partner at a16z?

The read between the lines is that a loud and dogmatic minority is the biggest short-term threat to the crypto industry. Politicians want easy praise, and if challenging criticism is all they’re going to get, they’ll drop what they’re doing for something else. As it happens, the opportunity cost of doing something else is non-trivial: Washington’s current pro-crypto sensibility may soon be challenged by a Democrat-heavy Congress or displaced by a new president with altogether different sympathies.

4. Oren Cass says Americans think crypto is a scam

Oren Cass, an influential thinker in the Republican orbit, thinks Republicans should ditch the crypto industry ahead of the midterms. Last year, the organization he founded, American Compass, conducted a poll with YouGov and asked 1,000 respondents what they thought of cryptocurrency. The upshot is that across genders, political parties, and economic classes, crypto is more likely to be understood as overhyped and a scam than exciting or important.

For Cass, being pro-crypto is politically unwise. As Donald Trump’s popularity sinks, and the Democrats try to gain control of Congress, pandering to the public will become more important than pandering to the crypto industry. “Perhaps the pandering to this particular special interest is lucrative,” wrote Cass, “but leaders hoping to build popular support for their agendas would be wise to focus elsewhere, or work actively to limit the damage from what has become a poorly understood online casino.”

The American mood is worth watching because Ottawa finds inspiration in the United States from time to time. It wasn’t until the U.S. moved on open banking that Canada decided to do the same. The Trump administration influenced Canada (and the rest of the world) to pause implementation of Basel banking-supervision rules. The GENIUS Act south of the border motivated Ottawa’s own attempt to regulate stablecoins via the Stablecoin Act.

Wonkier stuff

1. Tiff Macklem relays concerns about non-bank financial intermediation

In an expansive conversation with Kevin Carmichael, Tiff Macklem discussed what’s on everyone’s mind: geopolitical uncertainty and the future of multilateralism. He also discussed what few are thinking about but which is still important: the growth in non-bank financial intermediation. “We measure the regulated financial institutions very well. We have a lot of good data on them,” he told Carmichael. “We don’t have as good data [on non-bank financial institutions].”

In 2016, the Financial Stability Board established a working group to monitor and report on non-bank financial intermediation, or NBFI for short. NBFI refers to all financial activity that isn’t done by a central or private banks. For example, pension funds and insurance companies do NBFI. Since the 2008 financial crisis, NBFI has grown in economies around the world, raising questions about how risks could materialize and threaten financial stability.

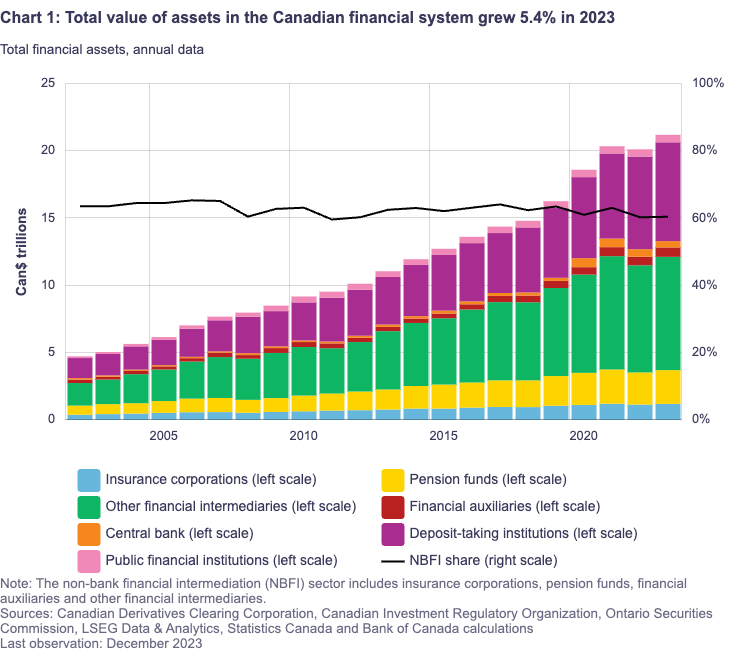

Last year, the Bank of Canada published what it had recently shared with the FSB’s working group on NBFI. The share of NBFI in Canada’s overall financial sector has remained relatively flat over the the past few decades.

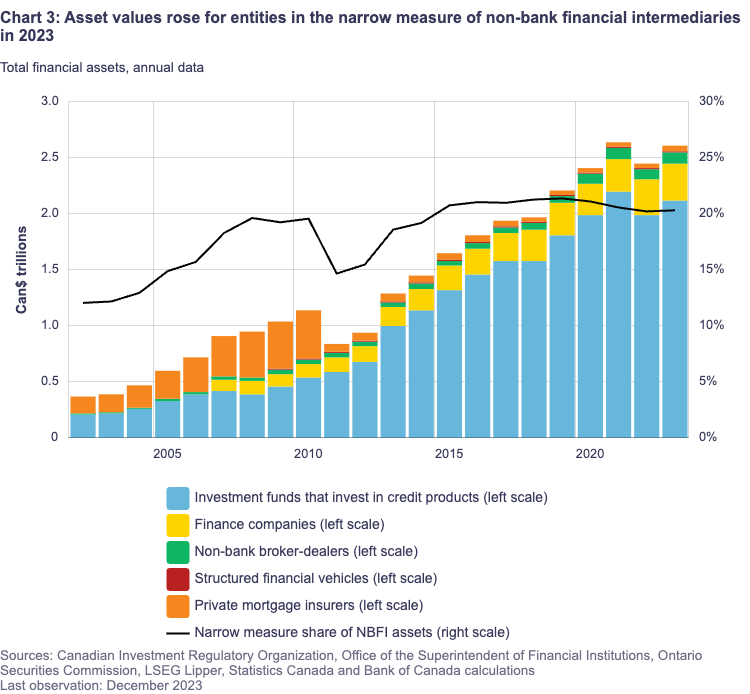

But zooming in tells another story. The narrower way to define NBFI is to only include non-bank financial intermediaries that engage in bank-like activities, such as investing customer “deposits” and making loans.

By the narrower definition, the level of NBFI is greater than it was in the lead up to the financial crisis of 2008. “These entities often provide a valuable alternative to traditional banking,” wrote Bank of Canada researchers. “However, these activities are often associated with financial leverage and represent an important channel through which risk can spread across the financial system.”

In the Bank of Canada’s most recent outlook on financial stability, NBFI is presented as an emerging risk, exacerbated by sudden shifts in trade policy and geopolitical chaos. I am eager for Bank of Canada’s next outlook to signal how this risk will compare to others that are sucking up so much oxygen right now, such as AI bubbles and threats to financial sovereignty.

Detours

1. Peak reaction to Mark Carney’s speech is far behind us

The reaction to Mark Carney’s speech at the World Economic Forum is itself evidence of the speech’s success. It invited a spectrum of reactions and on multiple dimensions—from praise to criticism, from within Canada as well as outside it, from academics and the commentariat to the people who just casually watch the news.

Stephen Maher, a Canadian journalist, wrote that this is what Carney meant when he said Canada would lead the world if the U.S. wouldn’t:

The impact was without precedent in Canadian history, says Raymond Blake, author of Canada’s Prime Ministers and the Shaping of a National Identity. “I cannot think of a speech from any other prime minister that had such an impact,” he told me on Wednesday. “Those are rare opportunities to capture international attention, and Carney knew that. He did not disappoint.”

The New York Times reported that his speech was met with a “rare” standing ovation.

Some academics looked past the prose to uncover what abstractions are animating the prime minister and how those may translate into foreign policy. For example, Kevin Bryan at the University of Toronto unpacked the “game theory realism” underlying the Carney Doctrine.

Though the reactions to Carney’s speech struck me as overwhelmingly positive, there were critics.

Tom Goldsmith wrote that Carney’s speech amounted to hypocrisy. For him, the Václav Havel reference was telling of Carney’s elitist diminution of the status of ordinary people:

Unlike Havel’s greengrocer taking their sign down, a bottom-up action of disobedience and disavowal of a broken system, for Carney, this moment calls for a top-down action from companies and statesmen, not the people. Actual people are notably missing from Carney’s framing.

Tyler Cowen wrote that Carney’s speech was, effectively, naive.

He had no solution to an immediately pending world where Canada is quite dependent on advanced AI systems from American companies (often, incidentally, developed by Canadian researchers in the U.S.). That is likely to be the next major development in this North American relationship, and it will not increase the relative autonomy of Canada or of any other middle powers.

Pierre Poilievre did something similar and then some. He said the Conservatives would propose a motion to pass the Canadian Sovereignty Act when the parliament returns next week.

Not everyone has to love the speech, but the critics are picking small fights. What is the point of a political speech like Carney’s, anyway? It’s not to satisfy everyone’s normative prejudices. It’s also neither to be self-defeating nor singlehandedly solve Canada’s problems. The point of a political speech is to move the right people at the right time in the right direction, where “right” is obviously in the eye of the person delivering the speech.

If judged in context, Carney’s speech is a lot like Kawhi Leonard’s jump shot for the Toronto Raptors against the Philadelphia 76ers in 2019. We could have debated Leonard’s moral character and commitment to the Raptors. We could have debated whether making that shot would have been enough to overcome the obstacles ahead. But those debates would have been irrelevant to the jump shot. The fact is Leonard made the bucket. And that was enough for the Raptors to have another shot at the NBA championship.