When social status is the answer to the innovator's dilemma

When social status is the answer to the innovator's dilemma

The history of financial services innovation shows us what it means to be human, and what to expect of the future

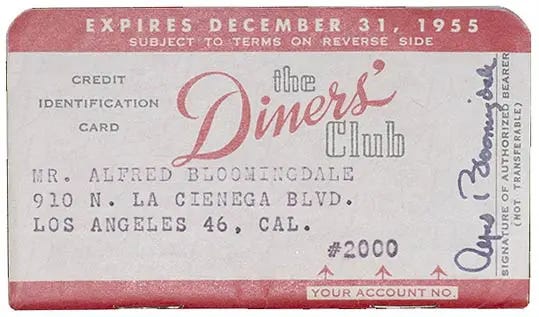

When the bill came for Frank McNamara, he reached for his pocket and discovered he hadn’t any cash on him. He was entertaining a business acquaintance one evening at Major Cabin’s Grill, a restaurant near the Empire State Building. The year was 1949, and so he couldn’t use a shiny plastic card or a slick payment app—these hadn’t come into existence yet. To avoid embarrassment, he phoned his wife and asked if she’d bring him some cash. While she drove to his rescue from Long Island, an idea struck McNamara. What if he had a card to which he could charge a bill from a restaurant anywhere in the city?

A year later, McNamara co-founded Diners Club. At the time, it was the closest thing to a universal credit card system the United States had ever seen. The antecedent to Visa and Mastercard and American Express, no good history of ways to pay neglects to mention Diners Club, as well as the inspiration behind it: McNamara’s little liquidity problem at Major Cabin’s Grill in 1949.

The only hitch is that this origin story is bullshit.

Every product needs a story

According to Matty Simmons, the first public relations person for Diners Club, the famous incident at Major Cabin’s Grill was fabricated. Simmons concocted the story because it sounded better than the truth. One day, McNamara simply came upon the idea and decided it was worth pursuing.

The big selling point wasn’t even the practical benefits, such as replacing a pocketful of cash. The most attractive benefit of having a Diners Club card would be the status it conferred upon the holder. “It’s having a good enough credit rating to own one of these cards so that restaurants will treat you like somebody who’s somebody,” McNamara explained in his pitch to Simmons. “If you’re a businessman and you’re entertaining clients or working on a deal, the people with you will be impressed.”

To launch, McNamara sent Diners Club cards, unsolicited, to thousands of prominent businesspeople, along with pamphlets extolling the benefits. Diners Club also convinced restaurants to accept the cards as payment by promising that their cardholders racked up bigger bills than people who paid with cash.

According to David Stearns, the practical benefits “were minor compared to the cultural meaning of the card: prestige.” At its peak, Diners Club had 1.3 million American cardholders, which was less than 1 percent of the United States’ population at the time.

Prestige has a powerful pull because we’re social animals. We are always doing things to improve our social status. We buy products that tell others impressive stories about ourselves, for example, or we make art to show others we’re talented. If you’ve been persuaded by such books as The Mating Mind, The Selfish Gene, or The Elephant in the Brain, then you already know we improve our social status to keep our genes around—or, more colloquially, to get laid.

McNamara understood that you had to move people on a visceral level to make them your customers. Promising practical benefits isn’t enough. More convenience. Lower prices. None of them means as much as prestige. Practical benefits fail to animate our base motivations as social animals. Prestige succeeds, which is why it was one of the more powerful forces that drove adoption of Diners Club cards and, after them, the credit cards we know and use today.

Social status is more important than ever before

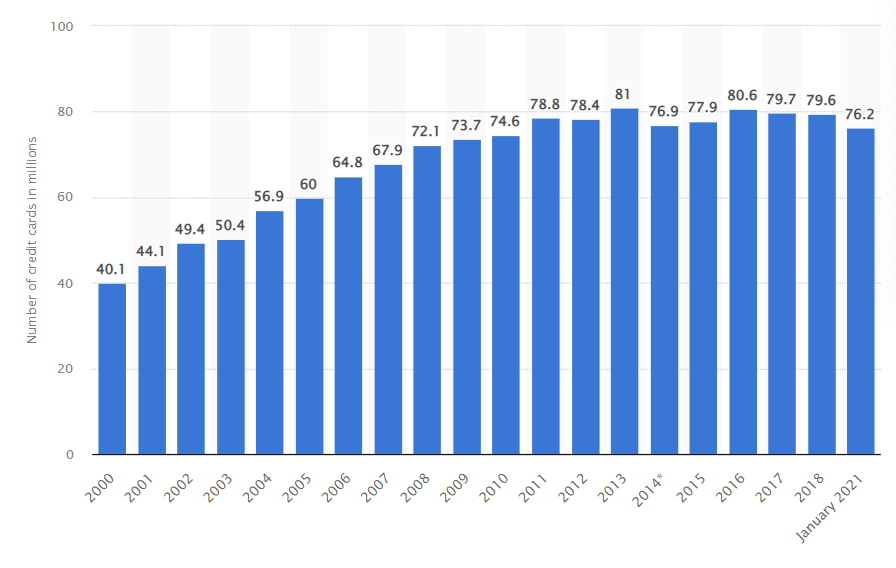

Fast forward to 2022. Now credit cards aren’t signs of social status. Thanks to Visa and Mastercard and American Express, as well as the banks that issue their cards, credit cards are accessible to almost everyone. Over the last several years, for example, the number of credit cards issued in Canada has exceeded the number of possible cardholders. Today, the average person has more than one credit card.

Figure 1. Millions of credit cards in Canada (source: Statista)

Credit cards became ubiquitous as part of a broader trend in financial services that started in the post-war era. According to Joe Nocera, that’s when financial services once reserved for the rich started becoming more accessible. It wasn’t just credit cards. It was mutual funds. It was cash management accounts. The middle class took a piece of the action, joining the ranks of the “money class.”

Though increasing access to financial services was good for everyone, it made things harder for today’s financial services innovators. Almost everyone has the same financial services, and so there’s little social status to absorb from having them. No one is bragging to the beautiful people at the party about their new digital wallet or “buy now, pay later.”

Nowadays, social status needs to come from somewhere other than the financial service being sold. The Diners Club card was, itself, a sign of social status. Today, it’s the tree that’s planted when you use your prepaid Visa card at the point-of-sale, signaling to others that you’re environmentally conscious and, therefore, enlightened. Or it’s the fees that are donated to a family in need when you open your RESP, signaling to others that you’re altruistic and, therefore, a good person.

I suspect that’s why cryptocurrency is all the rage. Despite its relative lack of practical benefits, cryptocurrency is promising a revolution. A circumvention of not only traditional financial institutions, but of our monetary system all the same. There’s something deeply philosophical about cryptocurrency, imbuing it with an aesthetic quality. Like the art you buy and show off, cryptocurrency in your portfolio signals to others who you are and what you’re about. In some circles, that you simply “get it” is a sign of prestige.

The fact is that social status is important when the products being offered seem the same. A bank account is a bank account. A credit card is a credit card. A no-fee trading account is a no-fee trading account. But imbue any of these with deeper meaning, an identity in which people want to wrap themselves, and they become something more.

Get ready for a wacky and wonderful world of financial services

Today’s innovators would be wise to take a page from the book of McNamara. McNamara understood the frictions of his financial services ecosystem. But he also understood what it means to be human—to want to climb the social hierarchy, and to use the narrative power of your financial services in that mission.

When you’re competing at the margin of social status, the boundaries of your relevant market get blurry. You’re no longer just selling financial services, competing with other financial institutions. You’re selling a way for someone to signal something to someone else. In the ring with just about every genre of company there is, it’s you against the world.

The competition is fierce. Even for people who like to show off their financial acumen by telling their friends about their high-interest savings account, financial services aren’t the only source of social status. People have many interests and peer groups. Social animals with finance on the brain may also like yoga, or coffee connoisseurship, or canoeing. If the practical benefits of new financial services aren’t an order of magnitude better than old financial services, social animals may find yoga classes, semiautomatic espresso machines, or canoe trips better uses of time and money. None of these is substitutable for the others until they compete at the margin of social status.

This means financial services are going to get not just better, but also cooler and weirder. The effect of the Internet has been to create a world of never-ending niches, as Ben Thompson has written, and so success “is about delivering superior quality in your niche.” What one niche finds cool, another will find weird. And what no niche finds weird, every niche will find boring. Roll your eyes, but I’m here for it. The possibilities are endless, and yet I still can’t get my crusty bank to issue me a credit card with The Death of Socrates on it.

My bank, my credit card network—that’s your cue, if you’re reading, to get on it. The rest of you—that’s your cue to acknowledge how low the bar is and get weirder.

If you found what you read interesting, please give it a like, share with your friends, or leave a comment. You can also respond to this email if you want to give me feedback.

An excellent analysis and great attempt to determine the "go forward". I for one never cared about the social status and refused to entertain cards that claimed "show that you have arrived".